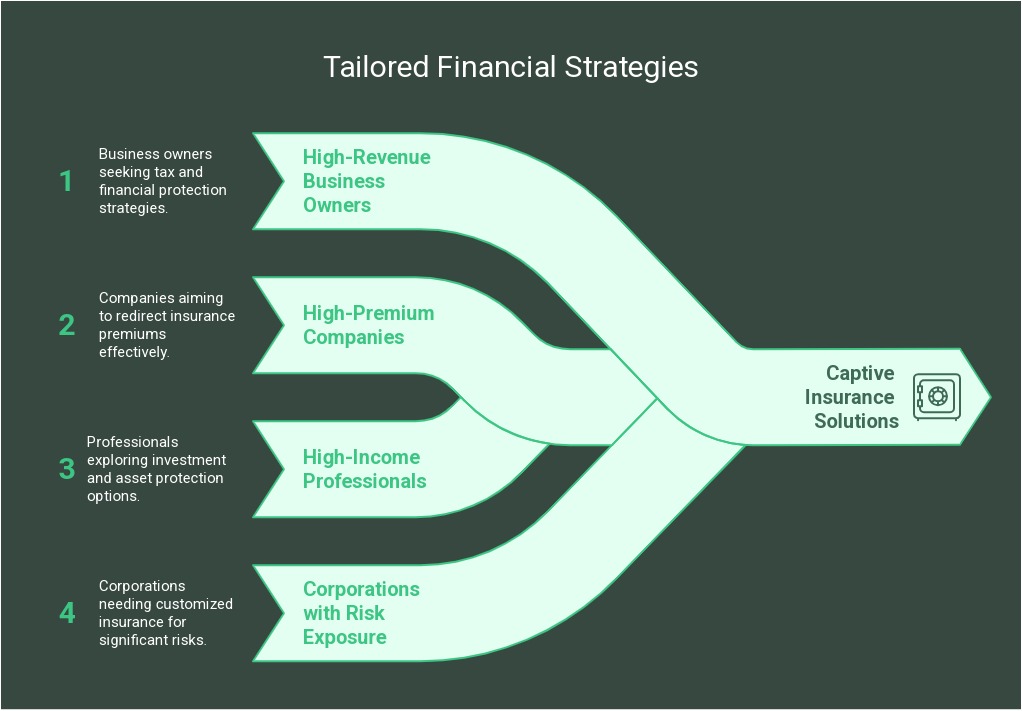

Captive insurance solutions for business tax savings and risk management

Discover how captive insurance solutions for business tax savings and risk management can help business owners lower tax liabilities, protect assets, and create long-term wealth. Learn how Fortune 500 companies use captive insurance to retain profits and reduce risks.

Captive Insurance Solutions for Business Tax Savings & Risk Management

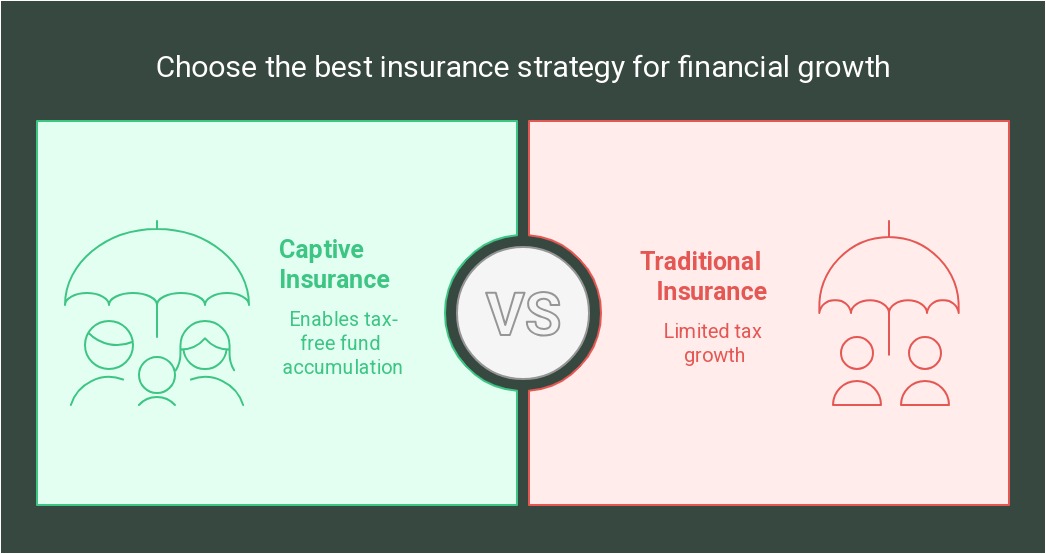

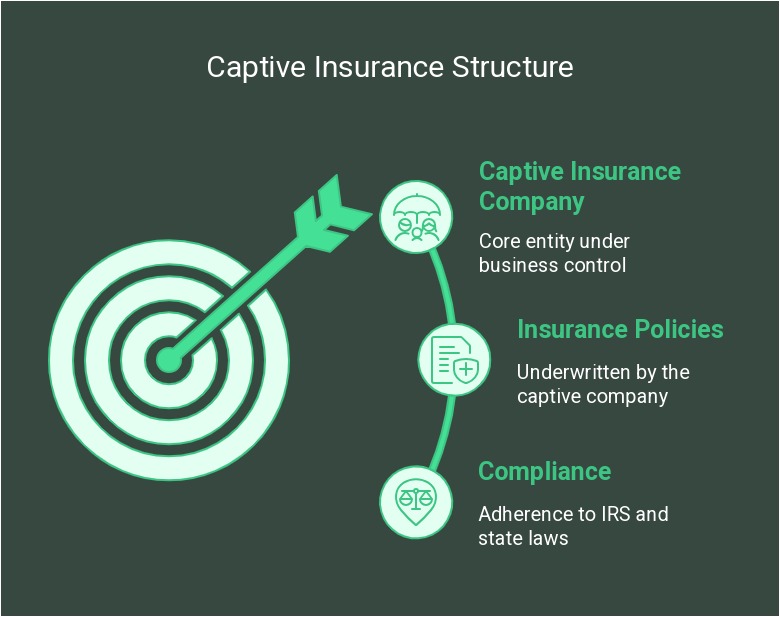

Captive insurance solutions for business tax savings and risk management allow business owners to take control of their risk while reducing tax liabilities and creating a tax-free wealth-building strategy.

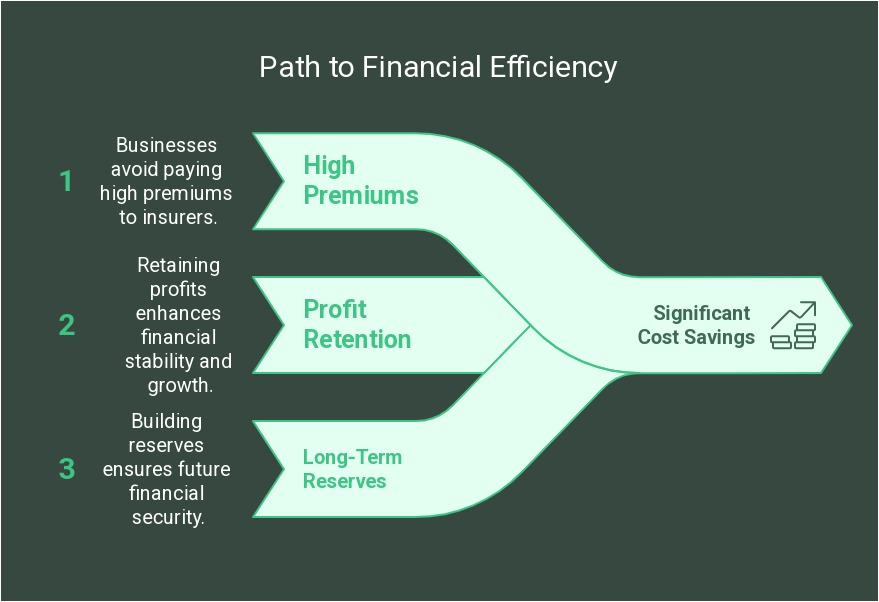

Did you know that Fortune 500 companies and large corporations operate their own private insurance companies to retain profits, reduce taxes, and self-insure against risk?

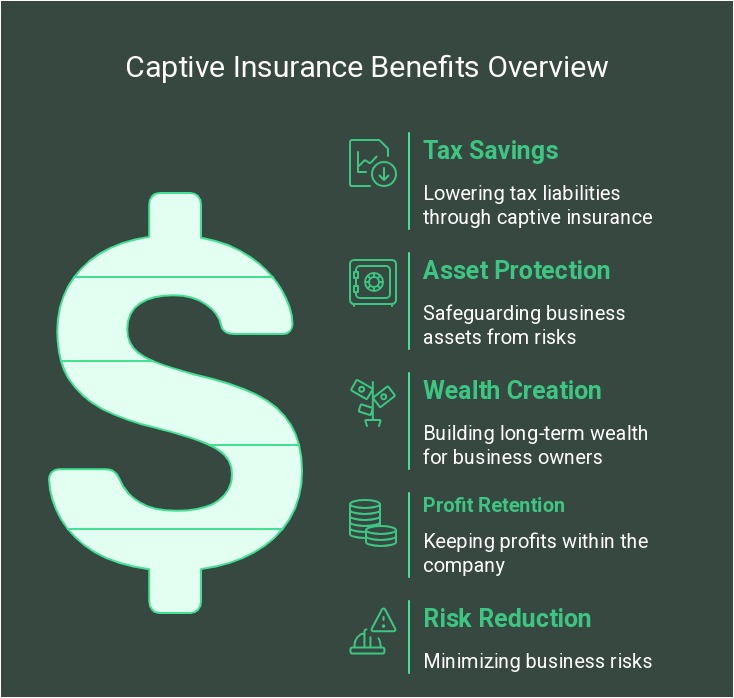

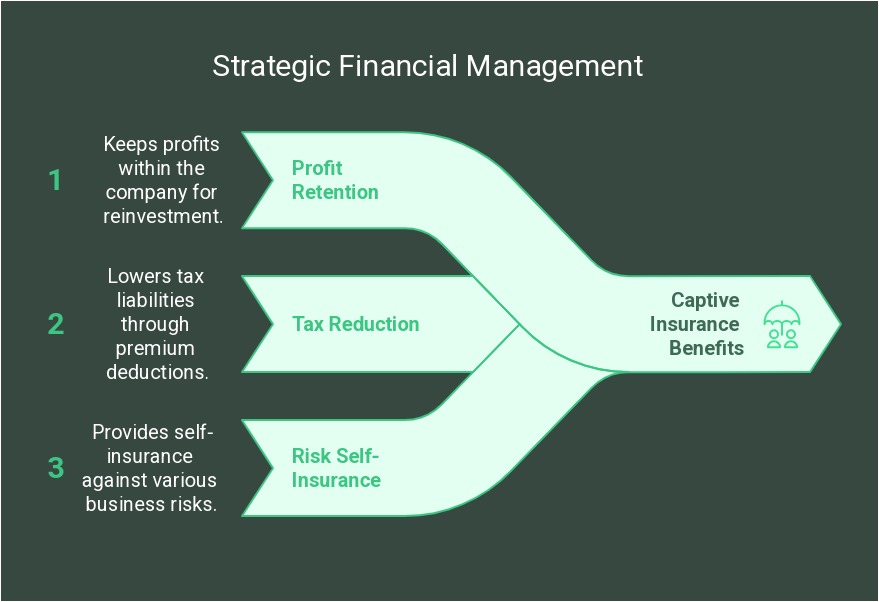

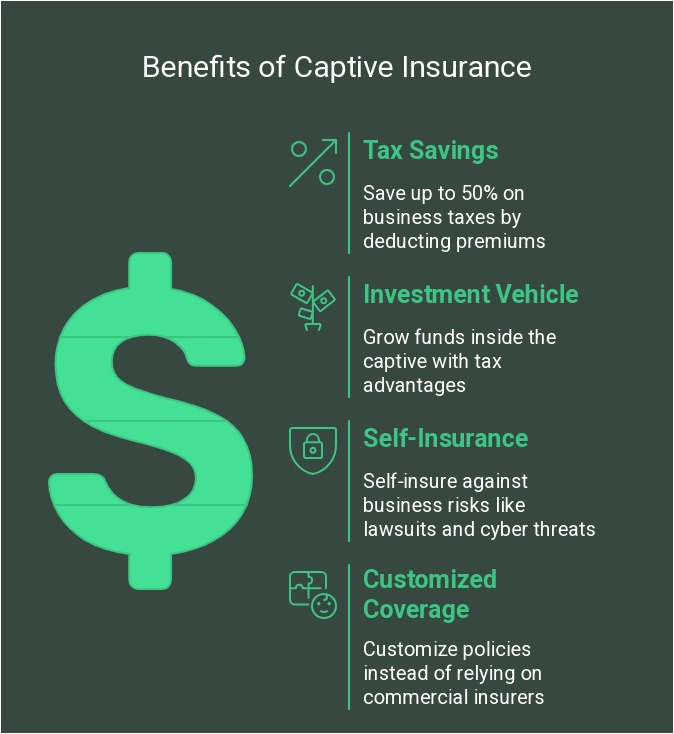

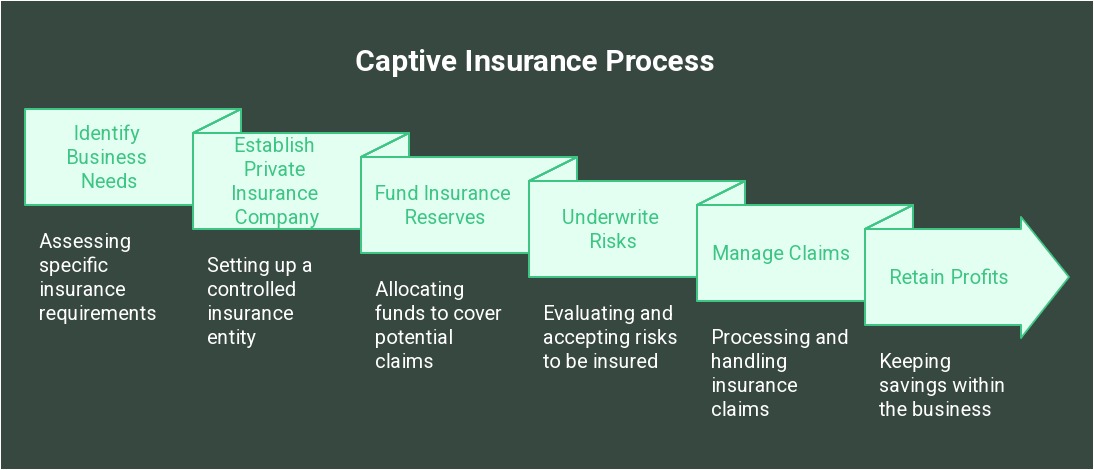

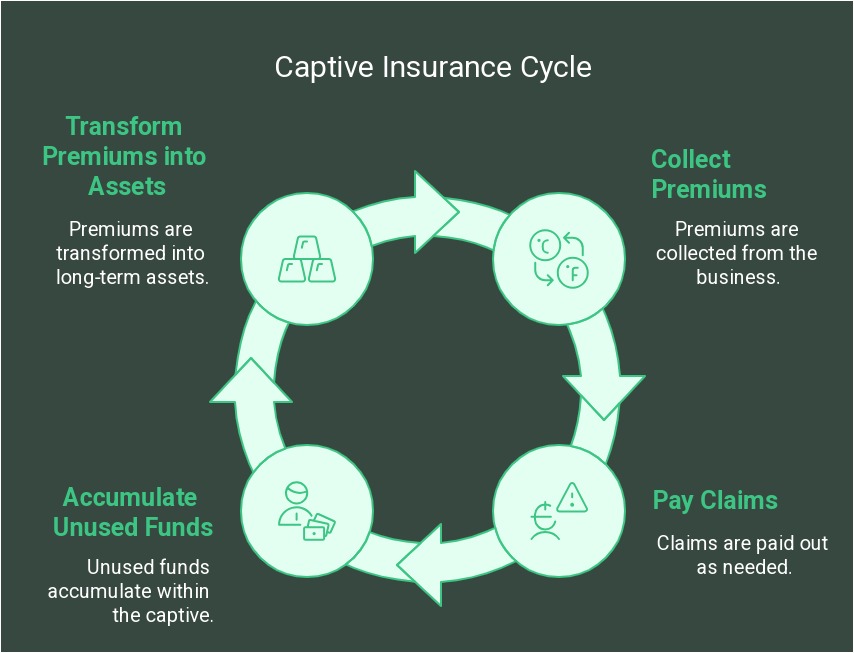

Captive insurance allows business owners to set up their own insurance company instead of relying on expensive third-party insurers. This strategy enables companies to:

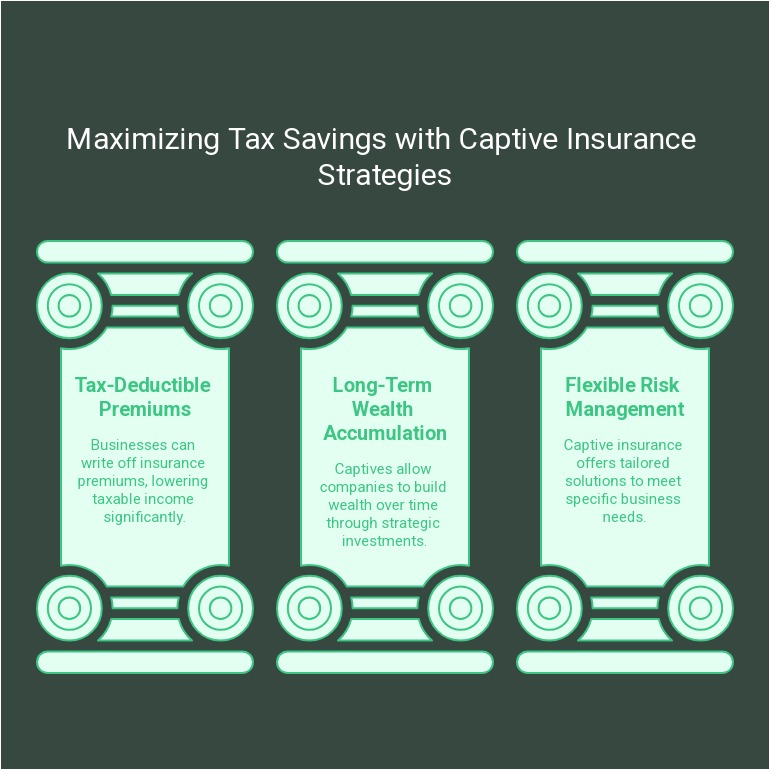

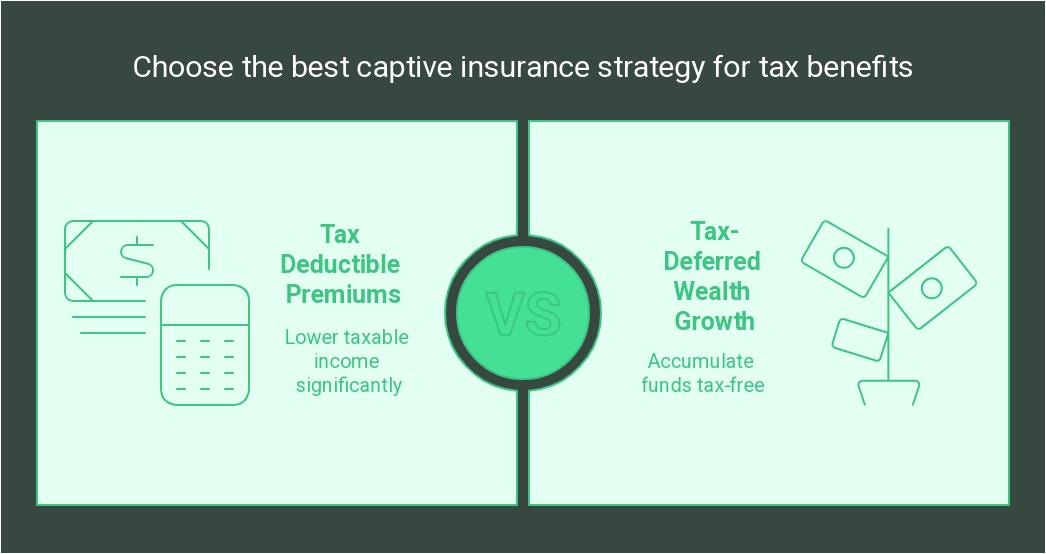

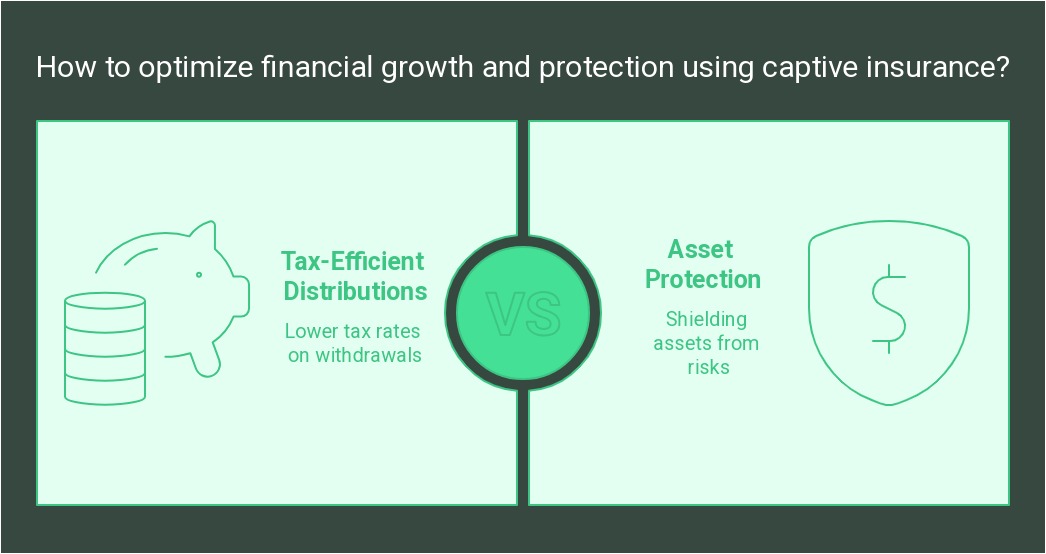

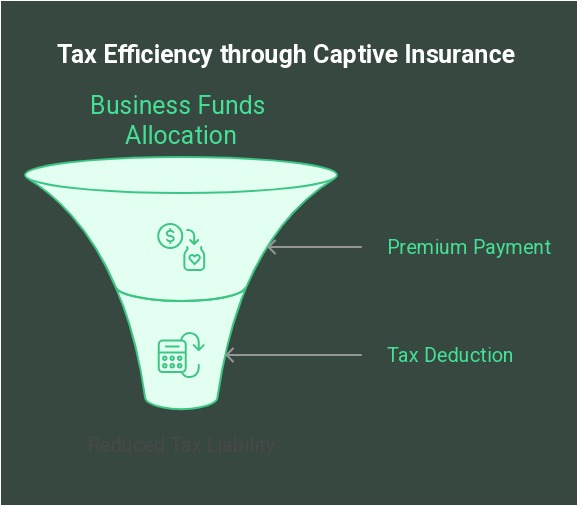

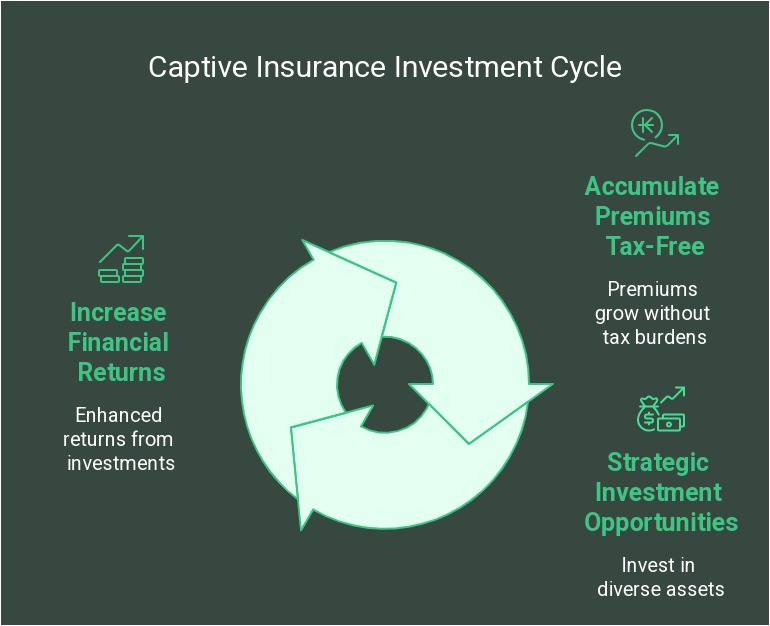

Save up to 50% on business taxes by deducting premiums paid into the captive as business expenses. Create a tax-free investment vehicle by growing funds inside the captive with tax advantages. Self-insure against business risks such as lawsuits, cyber threats, supply chain issues, and market volatility. Gain greater control over coverage by customizing policies instead of relying on commercial insurers with high fees and broad coverage gaps.

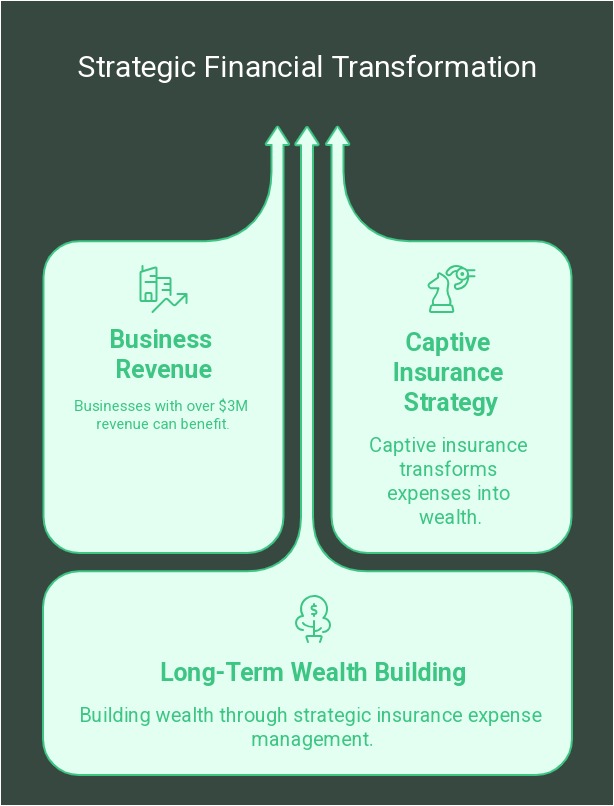

Captive insurance isn’t just for large corporations—businesses earning over $3M per year can leverage this strategy to transform insurance expenses into long-term wealth.